COLUMN: The rand has gone from strength to strength. A year ago, it was trading around R19 to the US dollar.

As I write this, it is closer to R16.50. That's a 14% strengthening over the past year.

So, what’s driving the rand, and what can we reasonably expect going forward?

Dollar normalisation, not collapse

Part of what we are seeing is continued unwinding of the US dollar.

When inflation peaked in 2022, aggressive rate hikes pushed the dollar to unusually strong levels. Now that inflation has eased, we have seen rates around the world come down and dollar normalisation.

Some commentators have been calling it dollar weakness, but I see it more as normalisation and nothing structural.

Local positives are a tailwind

A number of positive developments in South Africa are contributing to rand strength:

- Credit upgrade from S&P Global Ratings

- Eskom stability improvements

- South Africa being removed from the grey list

- A budget surplus - we’re currently collecting more tax than we’re spending, which makes us a more credible borrower

- A new SARB mandate - the South African Reserve Bank now officially targets 3% inflation, rather than a 3-6% band

That last point matters more than most people realise. The US targets 2% inflation.

Previously, the gap between SA and US inflation targets was as wide as 4%. It’s now closer to 1%. That’s a meaningful shift.

All of these factors help at the margin. None of them are easy to quantify, and none, in isolation, explain the magnitude of what we’ve seen.

What can we learn from history

The chart below shows the 26 year history of the rand versus the US dollar. I've highlighted the period from roughly 2000 to 2010.

During that period, the rand actually strengthened against the USD. The JSE generated about 15% a year for 10 years. It was a wonderful time.

Those were the Mbeki years where we ran account surpluses and our debt to GDP was very low.

We often give credit to Mbeki and Manuel for this period of prudence, but that may be overstating it. Much of the backdrop was a powerful commodity cycle.

At the time, the commodity sector was growing at close to 30% a year, which drove two things: a surge in tax revenue and a stronger rand.

Zuma was, in many ways, unlucky with timing. He took over in 2010 just as the cycle turned.

From about 2010 to 2020, commodities underperformed, tax collections weakened, budget deficits widened, and the rand depreciated at roughly 4-5% per year in line with South Africa's deteriorating balance sheet.

There was also massive state capture but let's not dwell on the past.

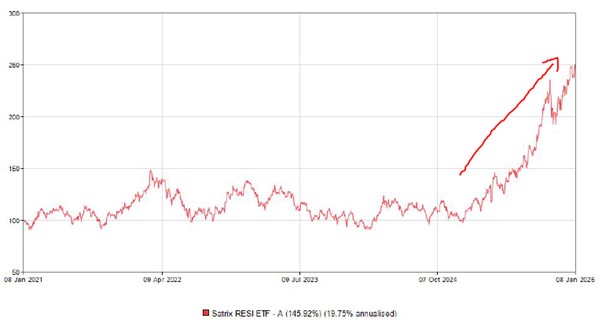

The commodity cycle

The point though is that the primary driver of rand strength back then was the commodity cycle.

With that in mind, have a look at the chart below. It shows performance of our commodity sector (I have used the Satrix Resi ETF as a proxy) - it’s up over 135% over the past year, and over the past 5 years, has generated a 19.75% annualised return.

Once again, we are running budget surpluses and the rand is strengthening.

How to think about the rand going forward

The current commodity run is still relatively young, having started around October 2024. It’s entirely possible that it lasts another decade, as it did in the 2000s.

If that happens, the rand could remain strong, or even strengthen further. It’s also possible that the cycle is shorter lived.

I like to think about the rand in the context of these long term cycles. They are almost impossible to time, and we never know how long they will last.

That said, I hope this one continues. It would bode very well for our stock market and the broader economy, including tax collections, employment, and fiscal surpluses.

From a portfolio perspective, it’s a reminder that as South Africans, our liabilities are in rands. Going all in offshore is risky. The right approach is a strategic split between local and offshore assets, based on personal circumstances.

I hope everyone had a fantastic December holiday, and I wish you a wonderful 2026. May we all see many all time market highs in the months ahead.

Matthew Matthee has a wealth management business that specialises in retirement planning and investments. He writes about financial markets, investments, and investor psychology. He holds a Masters Degree in Economics from Stellenbosch University and a Post Graduate Diploma in Financial Planning from UFS. [email protected]

‘We bring you the latest Garden Route, Hessequa, Karoo news’